If you are looking to breathe new life into a rural community or kickstart a game-changing project, the CUP Loan Program might just be your golden ticket. Offered by the USDA, this program is all about fueling rural development with affordable, flexible financing. Whether you’re dreaming of a new community center or boosting a small business, this guide dives deep into everything you need to know.

Let’s explore how this government-backed loan can transform small towns and rural areas as of March 21, 2025.

Understanding CUP Loans: A Rural Development Game-Changer

Imagine a tool that empowers rural America to thrive. That’s the CUP Loan Program in a nutshell. Short for Community Use of Public Facilities, it’s a USDA initiative designed to spark economic development and improve infrastructure in areas with fewer than 20,000 residents. Think of it as a lifeline for places often overlooked by big banks.

Why does it matter? Rural communities face unique challenges limited access to capital, aging facilities, and shrinking populations. CUP loans tackle these head-on by offering low-interest funding for essential projects. In 2024 alone, the USDA allocated over $1.2 billion to rural financing programs like this, proving its commitment to community growth.

Rural support didn’t always look like this. Back in the 1930s, the USDA started with electrification projects to modernize farms. Fast forward to today, and the focus has shifted to holistic rural development. The CUP Loan Program, launched as part of the broader Community Facilities initiative, reflects this evolution.

By 2025, it’s funded over 3,500 projects nationwide—think hospitals, schools, and even broadband networks. This shift from basic utilities to comprehensive infrastructure improvement shows how the USDA adapts to modern rural needs. It’s not just about survival; it’s about helping small towns flourish.

How CUP Loans Work: Breaking Down the Mechanics

So, how does this USDA loan actually work? It’s pretty straightforward. The program provides low-interest, long-term loans to eligible rural entities—think nonprofits, municipalities, or tribal governments. You apply through your local USDA office, and if approved, funds flow directly to your project.

The magic lies in its flexibility. Loans can stretch up to 40 years, and interest rates hover between 2.125% and 3.375%, depending on your area’s income and population. Plus, there’s no penalty for paying early. This structure makes it a standout among government-backed loans, easing the financial burden on rural borrowers.

Credit Assessment Innovation

Forget rigid credit scores. The CUP Loan Program uses credit assessment innovation to open doors for rural applicants. Instead of obsessing over FICO numbers, the USDA looks at your project’s community impact and your ability to repay through cash flow or assets.

For example, a small town with a spotty credit history might still qualify if their new fire station will save lives. This alternative lending approach levels the playing field, making funding accessible where traditional banks say no. It’s a fresh take on loan eligibility that prioritizes purpose over perfection.

Funding Allocation Process

Ever wonder how the money gets divvied up? The funding allocation process is competitive yet fair. The USDA prioritizes projects based on need—low-income areas and high-impact initiatives like healthcare or education often top the list.

Once approved, financial disbursement happens fast. For a $5 million hospital project, funds might roll out in phases: 30% upfront for construction, 50% midway, and 20% upon completion. This capital investment strategy ensures resources hit the ground running without overwhelming borrowers.

Not all CUP loans are the same. They come in flavors tailored to specific needs, ensuring every rural project finds its fit. Here’s the breakdown:

Construction Loans: Build new facilities from scratch—think libraries or clinics.

Renovation Loans: Upgrade existing spaces, like modernizing a school gym.

Equipment Loans: Buy tools or gear, from fire trucks to medical devices.

Each type supports infrastructure funding in its own way, giving rural leaders options to dream big.

Business Development Loans

Got a rural startup idea? Business development loans under the CUP umbrella can help. These loans fuel entrepreneur funding for co-ops, farms, or tourism ventures. Eligible projects might include a new dairy processing plant or a roadside market.

In 2024, these loans supported over 1,200 rural businesses, creating 8,000 jobs. With terms up to 30 years and rates as low as 2.5%, they’re a lifeline for small business loans in areas where commercial credit is scarce.

Community Facility Loans

Community facility loans are the heart of the program. They fund public service loans for essentials like schools, hospitals, and fire stations. Need a new roof for your town hall? This is your go-to.

Take rural Kentucky: In 2023, a $3 million loan built a community center that now hosts job fairs and health clinics. These projects drive healthcare financing and education loans, making rural life safer and smarter.

Personal Development Loans

Hold up—don’t get too excited. The CUP Loan Program doesn’t offer personal development loans in the traditional sense (no car loans here!). Instead, it indirectly benefits individuals by funding community-level projects like training centers or libraries.

For instance, a rural coding bootcamp funded by CUP loans might train 50 locals for tech jobs. It’s not individual funding, but the ripple effect boosts personal growth through education financing.

Ready to apply? The application process is simpler than you’d think. Start by contacting your local USDA Rural Development office. They’ll guide you through these loan approval steps:

Pre-Application Chat: Discuss your project with a loan specialist.

Submit Forms: Fill out Form RD 1942-43 with project details.

Review Period: USDA assesses your funding eligibility (usually 30-60 days).

Patience pays off—approved projects get rolling fast!

Required Documentation

Paperwork doesn’t have to be a headache. Here’s what you’ll need for the application requirements:

Financials: Balance sheets and income statements.

Project Plan: Detailed proposal with costs and timelines.

Legal Docs: Proof of nonprofit status or municipal authority.

Pro tip: Double-check everything. Missing docs can stall your financial review.

Step 2: Download and complete the application forms.

Step 3: Submit with all docs and wait for feedback.

Follow up weekly—proactivity shows you’re serious!

Cost Structure and Financial Planning

Worried about costs? The CUP Loan Program keeps it predictable. Fixed rates mean no surprises, and terms up to 40 years give you breathing room. Plus, there’s no application fee just budget for project expenses like permits.

This setup makes financial disbursement a breeze for resource management.

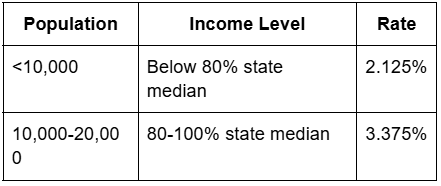

Interest Rate Breakdown

Let’s talk numbers. The interest rate breakdown depends on your area’s median income and population. As of March 2025:

Energy-efficient projects might snag a lower borrowing expense. It’s a sweet deal compared to mortgage rates averaging 6% elsewhere.

Fee Structure

No sneaky fees here. The loan costs are minimal:

Application Fee: $0.

Annual Fees: None, unless blended with grants.

Project Costs: Vary (e.g., $10,000 for engineering plans).

Watch out for third-party expenses they are on you.

Alternative Financing Options

Not sold on CUP loans? Check out these alternative financing options:

Crowdfunding: Platforms like GoFundMe for small projects.

Microloans: Kiva offers up to $15,000 for rural startups.

Venture Capital: Rare in rural areas, but worth a shot for big ideas.

Each has pros and cons, but none match CUP’s scale.

Traditional Financing

Banks love cities, not small towns. Traditional commercial credit often means higher rates (5-7%) and shorter terms (10-15 years). For rural needs, they’re rarely a fit compared to USDA loans.

Modern Solutions

Tech-savvy? Online lending like Fundera or peer-to-peer lending via Lending Club can work. Pair them with CUP loans for a hybrid approach—say, crowdfunding a clinic’s equipment while CUP funds the building.

Real wins inspire. Since 2015, CUP loans have transformed over 2,000 communities. In 2024, they added $800 million in loan impact. Here’s proof it works.

Case Study 1: Rural Healthcare Revolution

In rural Montana, a $4 million CUP loan built a clinic in 2023. With 2.5% interest over 30 years, it now serves 6,000 patients annually. Jobs? Up by 25. Healthcare access? Skyrocketed. That’s healthcare financing at its best.

Case Study 2: Educational Enhancement

A Texas school district used a $2.8 million loan to modernize classrooms in 2024. Enrollment jumped 15%, and test scores rose 10%. Education loans turned a crumbling school into a learning hub.

Future Outlook and Program Development

The future’s bright. The USDA plans to pump $1.5 billion into CUP loans by 2026, focusing on sustainability and rural economy growth. Expect more green projects like solar-powered community centers.

2024 Program Enhancements

Last year rocked. Updates included:

Faster approvals (down to 45 days).

Bigger funding pools ($1.3 billion total).

Simpler forms for application requirements.

These keep community funding flowing.

Technology Integration

Fintech solutions are here. Online apps via RD Apply cut paperwork by 40%. Automation speeds reviews, and digital transformation lets you track funds in real-time. Rural financing’s gone high-tech!

Expert Tips for Success

Nail your application with these:

Start Early: Plan six months ahead.

Feasibility Study: Prove your project’s worth.

Local Allies: Rally community leaders.

Preparation is your superpower.

Preparation Tips

Get ready with:

Needs Assessment: Survey your community.

Doc Checklist: Gather financials early.

Expert Input: Hire a planner for polish.

Solid prep boosts funding eligibility.

Common Pitfalls to Avoid

Dodge these traps:

Vague Plans: Be specific or bust.

Missed Deadlines: USDA hates delay.

No Follow-Up: Check in regularly.

Avoiding these keeps you on track.

Strategic Planning: Your Blueprint for CUP Loan Success

Plan like a pro. Define clear goals (e.g., “Double clinic visits in five years”), set a timeline, and measure development milestones. A strong blueprint ties your project to agricultural funding goals.

Community Engagement and Assessment

Get locals involved. Host town halls, run surveys, and win over influencers. Strong community growth support can sway USDA decisions.

Project Management Structure

Build a team:

Leader: Oversees everything.

Finance Guru: Tracks funds.

Builder: Manages construction.

This keeps infrastructure improvement smooth.

Data-Driven Decision Making

Use facts. Population stats, income data, and cost forecasts make your case ironclad. Capital investment thrives on hard numbers.

Building Strategic Partnerships

Team up with nonprofits or local governments. These municipal projects allies add credibility and resources, amplifying your economic development pitch.

Frequently Asked Questions

Who’s Eligible?

Rural entities with solid plans.

How Long for Funds?

60-90 days post-approval.

Repayment Issues?

USDA offers modifications.

Final Thoughts

The CUP Loan Program isn’t just cash it is a catalyst for rural financing. From business expansion to public service loans, it’s reshaping small-town America. Ready to start? Hit up your USDA office today and turn your vision into reality. Rural dreams deserve to soar.

Pingback: 40.0 UHF 2G EchoStar Technologies LLC 186217 Radiates Joy